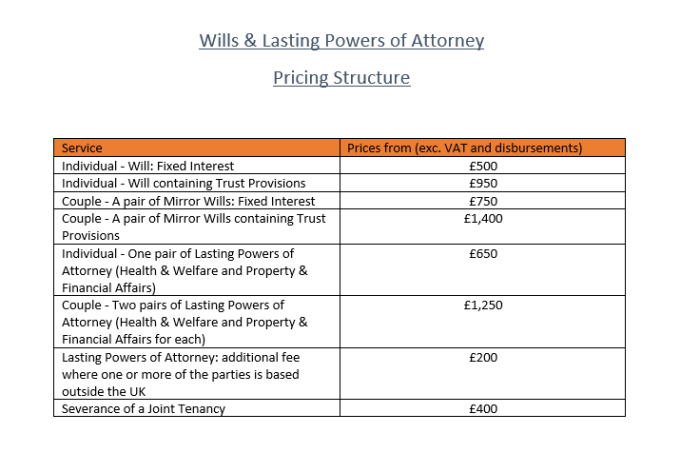

Creating a Will.

In most cases we offer a fixed fee for writing your Will. On this page you will find examples of the most common types of Will that we write for our clients, and the fees associated.

Everybody’s circumstances are unique to them. You can be confident that your Will can be tailored to fit your wishes and personal situation.

Please contact us if you would like advice on what is right for you.

Scroll down

Lasting Powers of Attorney

Lasting Powers of Attorney are the means by which you give someone you that you trust the power to make decisions for you.

The person to whom you grant that power is called your attorney.

A Health & Welfare LPA can only be used by your attorney when you have lost the mental capacity to make those decisions yourself. With a Property & Financial Affairs LPA, you can decide whether your attorney(s) can use it as soon as it’s registered, or only when you have lost mental capacity.

Examples of clients that we have helped

Our STEP-qualified solicitors can give practical tax planning advice to a wide range of individuals. Here are some examples of clients that have sought assistance from the Estate Planning team at Foxfield.

Blended family seeks assurance their children are protected

We were approached by Mr. and Mrs. V; a married couple, each with children from a previous relationship. They wanted to make provision for the survivor of them but also planned to ensure that their respective children would inherit when the survivor dies. They were concerned that if they had Wills leaving everything to each other on the first death, the survivor could change their Will thereby defeating the interests of the children of the first to die.

We prepared them a pair of Wills incorporating life interest trust provisions to take effect on the first death. The trust will provide an income stream to the survivor but will protect the underlying capital, which passes to the children on the second death. The survivor will retain the right to occupy the home or its replacement during his or her lifetime. As the assets will never form part of the survivor’s estate, they will be unaffected by any changes the survivor might make to their own Will in the future. There is therefore no risk that the children of the first to die will lose their inheritance as a result of their step parent re-writing his or her Will after the first death.

The cost of this work was £1,400 + VAT

Potential unsuitability of beneficiaries

We were instructed by Mr and Mrs C, who wanted to have Wills which would provide for their three children. Whilst they would ideally wish to divide their estate equally between their adult children, they were concerned that it would not be safe for the children to inherit under the current circumstances. Their eldest son had been unfortunate in business and was being chased by creditors; bankruptcy remained a real possibility. Their middle child was something of a spendthrift and likely to squander large sums of capital. Their youngest lacked motivation and they were concerned that a windfall might further diminish his efforts to enter the workplace.

This was a situation which lent itself to flexible Wills, by which the estate is distributed at the discretion of the trustees. The trustees can assess the landscape when the time comes and make distributions as and when it is safe to do so. This will protect the eldest from third party claims, avoid the risk that the middle child becomes a victim of his own extravagance and ensure the youngest remains motivated. If and when the various hazards recede, it may be possible to pay out the trust fund equally between the children. The preparation of a pair of Wills with discretionary trust provisions, supported by letters of wishes, helps ensure the timing is right.

The cost of this work was £1,400 + VAT

Providing assistance to a disabled family member`

We were contacted by Mr. and Mrs. M, a couple with an only child who is in receipt of Child Disability payment. It was unlikely that their daughter would ever be able to live independently or support herself financially. They were wealthy and had assets well in excess of the Inheritance Tax threshold. They wanted mirror Wills whereby the survivor would inherit outright on the first death with the bulk of their estate left on discretionary trust for their daughter. They did however wish to leave an amount to charity on the second death. They accepted that there would be a charge to Inheritance Tax on the second death but were concerned about the periodic 10 yearly and exit charges that normally apply to discretionary trusts.

In accordance with their wishes, we prepared Wills which leave everything to the survivor on the first death. The survivor’s Will leaves a legacy equivalent to 10% of the net residuary estate to charity. This reduces the rate of tax on the residuary estate from 40% to 36%. The Will provides that the survivor’s residuary estate will be left on trusts which qualify for special inheritance tax treatment. This will mean that the daughter’s interests are protected for the rest of her life by a group of trustees. It also means that the estate will face a smaller inheritance tax bill. This kind of qualifying trust for a disabled person is one where all payments must go to the disabled person, except for up to £3,000 per year (or 3% of the assets, if that’s lower), which can be used for someone else’s benefit.

The cost of this work was £1,400 + VAT

Avoiding Inheritance Tax by making gifts to children

Mr and Mrs C approached us wanting to update their Wills. They are married and had Wills leaving their estate to each other and then equally to their three children on the second death. They had income and capital well in excess of their needs and wished to reduce the taxable value of their estates by making lifetime gifts. Their children were all over 18 but they considered them too young to inherit substantial sums. Mr. and Mrs. C were aware of the requirement to survive gifts by 7 years in order for them to fall out of their estate for Inheritance tax purposes. They had significant cash deposits and a share portfolio which had risen significantly in value over the years. They wanted to know how get the gifting process underway without making direct gifts to the children.

We assisted the couple in establishing lifetime discretionary trusts for the next generation and beyond. They had not made any gifts within the last 7 years and so they could each gift an amount up to the Nil Rate Band (£325,000), thereby avoiding a lifetime charge to Inheritance Tax. They will be able to repeat this process every 7 years. They cannot benefit themselves from the trusts but they were able to appoint themselves as trustees. This means they can manage the trust investments and determine when the beneficiaries receive distributions from the trust. They will fund the two trusts with cash because their share portfolio has risen in value and they do not wish the gift in to trust to trigger a Capital Gains Tax liability.

The cost of this work was £1,750 + VAT